Introduction

During the last few years of my career I have had the opportunity to work in two of the major fields of practice for actuaries – life insurance and non-life insurance. Something that always bothered me is that actuaries who perform reserving work in either of these two areas use totally different techniques from each other.

Life actuaries will generally build cash-flow models to project out expected income and outgo to derive the expected profit for each policy they are called on to reserve for, which is then discounted back to produce the reserve amount. One of the key inputs into this type of reserving model is a life table which tabulates mortality rates which apply to the insured population that is being reserved for.

Non-life actuaries, on the other hand, almost never build cash-flow models, but will apply a range of techniques to past claims information (arranged into a “triangle”, see later in the post for a famous example) to derive expected claims amounts that are held as an incurred but not reported reserve (IBNR). Some of these techniques are the chain-ladder, the Bornhuetter-Ferguson (Bornhuetter and Ferguson 1973) and Cape-Cod techniques (Bühlmann and Straub 1983). Lifetables are never considered.

It would make sense intuitively that there is some connection between these two “tribes” of actuaries who, after all, are both trying to do the same things, but for different types of company – make sure that the companies have enough funds held back to fund claims payments. This post tries to illustrate that in fact, hidden away in the chain-ladder method, there is an implicit life table calculation and that IBNR calculations can be cast in a life table setup. The key idea was actually expressed in a paper I wrote for the 2016 ASSA convention with Professor Rob Dorrington and appeared as an appendix in the paper.

Something else that the idea helps with is that it provides an explanation why the chain-ladder is so popular and seems to work well. The chain-ladder method remains the most popular choice of method for actuaries reserving for short term insurance liabilities globally and in South Africa (Dal Moro, Cuypers and Miehe 2016). Although stochastic models have been proposed for the chain-ladder method by Mack (1993) and Renshaw and Verrall (1998), the underlying chain-ladder algorithm is still described in the literature as an heuristic, see for example Frees, Derrig and Meyers (2014).

The simple explanation for the success of the chain-ladder method is that underlying the estimates of reserves produced by the chain-ladder method is a life table and that the chain-ladder method is actually a type of life-table estimator.

The rest of the post shows the simple maths and some R code to “pull out” a life table for the chain-ladder calculation. In a future post, I hope to discuss some other helpful intuitions that can be built once the basic idea is established.

The code for this post is available on my GitHub account here:

Chain-ladder calculations

Define:

![]()

as the claims amount relating to accident year i in development period J, where there are I accident years and J development years. An example claims triangle is shown below, that appears in Mack (1993). This triangle can easily be pulled up in R by running the following code that references the excellent Chainladder package:

[sourcecode language=”r”]

require(ggplot2)

require(ChainLadder)

require(data.table)

require(reshape2)

require(magrittr)

GenIns

[/sourcecode]

| i | C(i,1) | C(i,2) | C(i,3) | C(i,4) | C(i,5) | C(i,6) | C(i,7) | C(i,8) | C(i,9) | C(i,10) |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 357 848 | 1 124 788 | 1 735 330 | 2 218 270 | 2 745 596 | 3 319 994 | 3 466 336 | 3 606 286 | 3 833 515 | 3 901 463 |

| 2 | 352 118 | 1 236 139 | 2 170 033 | 3 353 322 | 3 799 067 | 4 120 063 | 4 647 867 | 4 914 039 | 5 339 085 | |

| 3 | 290 507 | 1 292 306 | 2 218 525 | 3 235 179 | 3 985 995 | 4 132 918 | 4 628 910 | 4 909 315 | ||

| 4 | 310 608 | 1 418 858 | 2 195 047 | 3 757 447 | 4 029 929 | 4 381 982 | 4 588 268 | |||

| 5 | 443 160 | 1 136 350 | 2 128 333 | 2 897 821 | 3 402 672 | 3 873 311 | ||||

| 6 | 396 132 | 1 333 217 | 2 180 715 | 2 985 752 | 3 691 712 | |||||

| 7 | 440 832 | 1 288 463 | 2 419 861 | 3 483 130 | ||||||

| 8 | 359 480 | 1 421 128 | 2 864 498 | |||||||

| 9 | 376 686 | 1 363 294 | ||||||||

| 10 | 344 014 |

The chain-ladder algorithm predicts the next claims amount in the table:

![]()

as:

![]()

where f is the so called loss development factor in development period j.

The volume weighted estimator of the loss development factor is defined in Mack (1993) as:

The estimate of the ultimate claims – the claims amount after all of the claims development is finished – for accident year i is given by:

![]()

In R, most of the chain-ladder calculations have been helpfully automated. To produce the loss development factors and an estimate of the IBNR, one runs the following code:

[sourcecode language=”r”]

fit = ChainLadder::MackChainLadder(GenIns)

plot(fit)

[/sourcecode]

Estimating the life table

Now for the lifetable. The percentage of claims developed by development period j is defined as:

and the percentage of claims developed in period j is:

and the percentage of claims developed in period j is:

![]()

The claims development can be cast in demographic terms as follows. Assume that for each accident year i, a population of claims:

![]()

will eventually be reported. In each development period j:

![]()

of the claims will be reported, or will “die”. The term is therefore comparable to the demographic quantity:

![]()

which is the probability of death in the period j, after surviving to time j. A full lifetable can then be derived from:

![]()

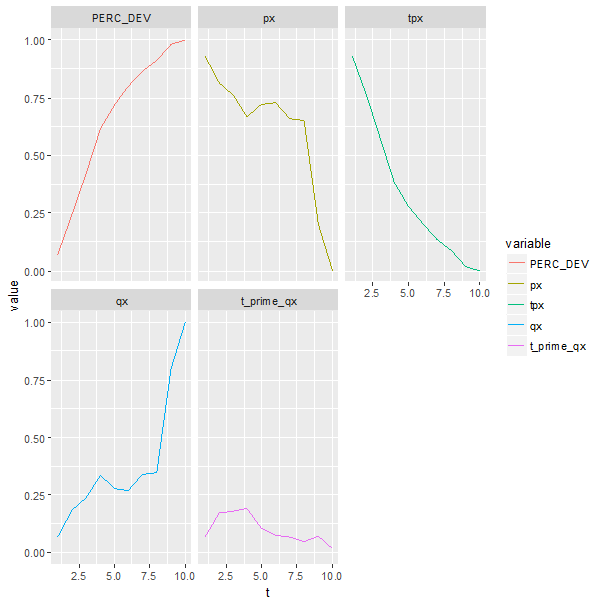

This is shown in the next table and plot, followed by the R code to produce the numbers.

| j | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|

| C(i,j+1) | 11 614 543 | 17 912 342 | 21 930 921 | 21 654 971 | 19 828 268 | 17 331 381 | 13 429 640 | 9 172 600 | 3 901 463 | |

| C(i,j) | 3 327 371 | 10 251 249 | 15 047 844 | 18 447 791 | 17 963 259 | 15 954 957 | 12 743 113 | 8 520 325 | 3 833 515 | |

| f(j) | 3.49 | 1.75 | 1.46 | 1.17 | 1.10 | 1.09 | 1.05 | 1.08 | 1.02 | 1.00 |

| F(j,J) | 14.45 | 4.14 | 2.37 | 1.63 | 1.38 | 1.25 | 1.15 | 1.10 | 1.02 | 1.00 |

| tq0 | 0.07 | 0.24 | 0.42 | 0.62 | 0.72 | 0.80 | 0.87 | 0.91 | 0.98 | 1.00 |

| t|q0 | 0.07 | 0.17 | 0.18 | 0.19 | 0.11 | 0.07 | 0.07 | 0.05 | 0.07 | 0.02 |

| qx | 0.07 | 0.19 | 0.24 | 0.33 | 0.28 | 0.27 | 0.34 | 0.35 | 0.80 | 1.00 |

| tpx | 0.93 | 0.76 | 0.58 | 0.38 | 0.28 | 0.20 | 0.13 | 0.09 | 0.02 | – |

| px | 0.93 | 0.81 | 0.76 | 0.67 | 0.72 | 0.73 | 0.66 | 0.65 | 0.20 | – |

[sourcecode language=”r”]

t_prime_qx = c(PERC_DEV[1], diff(PERC_DEV))

max_age = length(PERC_DEV)

px = numeric(10)

tpx = numeric(10)

qx = numeric(10)

px[1] = (1-t_prime_qx[1])

tpx[1] = px[1]

qx[1]= t_prime_qx[1]

for (i in 2:length(PERC_DEV)){

print(i)

qx[i] = t_prime_qx[i]/tpx[i-1]

px[i] = (1-qx[i])

tpx[i] = tpx[i-1]* px[i]

}

lifetable = data.table(t = seq(1,max_age), PERC_DEV=PERC_DEV,px = px, tpx=tpx, qx=qx,t_prime_qx=t_prime_qx )

lifetable_melt = lifetable %>% melt(id.var="t") %>% data.table()

lifetable_melt %>% ggplot(aes(x=t, y=value)) + geom_line(aes(group = variable, colour = variable)) + facet_wrap(~variable)

[/sourcecode]

Conclusion

When will the above calculations work well? These calculations make sense when dealing with triangles that increase monotonically i.e. do not allow for over-reserving or salvage and recoveries. A good example is on count triangles of paid claims.

Now that we have shown that the chain-ladder estimates a lifetable, the question is whether this is just an interesting idea that lets one connect two diverse areas of actuarial practice, or if any significant insights with practical implications can be derived. That will be the subject of the next post.

References

Bornhuetter, R. and R. Ferguson. 1973. “The Actuary and IBNR”, Proceedings of the Casualty Actuary Society Volume LX, Numbers 113 & 114

Bühlmann, H. and E. Straub. 1983. “Estimation of IBNR reserves by the methods chain-ladder, Cape Cod and complementary loss ratio,” Paper presented at International Summer School. Vol. 1983:

Dal Moro, E., F. Cuypers and P. Miehe. 2016. Non-life Reserving Practices. ASTIN.

Frees, E.W., R.A. Derrig and G. Meyers. 2014. “Predictive Modeling in Actuarial Science”, Predictive Modeling Applications in Actuarial Science 1:1.

Mack, T. 1993. “Distribution-free calculation of the standard error of chain-ladder reserve estimates”, Astin Bulletin 23(02):213-225.

Renshaw, A.E. and R.J. Verrall. 1998. “A stochastic model underlying the chain-ladder technique”, British Actuarial Journal 4(4):903-923.